In this week’s blog post, I will be comparing two of the leading pharmacy chains in the United States – CVS and Walgreens. Using fundamental data, we will determine which one of these two stocks is superior. I will start off by talking about the company overview, and then perform the fundamental analysis on each stock. Let’s dive in.

Company Overview

CVS Health Corporation (CVS) – CVS Health Corporation provides health services and plans in the United States. Its Pharmacy Services segment offers pharmacy benefit management solutions, such as plan design and administration, formulary management, retail pharmacy network management, mail order pharmacy, specialty pharmacy and infusion, Medicare Part D, clinical, disease management, and medical spend management services. The company’s retail segment sells prescription drugs and general merchandise, such as over-the-counter drugs, beauty products, cosmetics, and personal care products, as well as provides health care services through its MinuteClinic walk-in medical clinics. Its Health Care Benefits segment offers traditional, voluntary, and consumer-directed health insurance products and related services, including medical, pharmacy, dental, behavioral health, medical management, Medicare plans, PDPs, Medicaid health care management services, workers’ compensation administrative services, and health information technology products and services. The company’s customers include employers, insurance companies, unions, government employee groups, health plans, Medicare Part D prescription drug plans, Medicaid managed care plans, plans offered on public health insurance exchanges and private health insurance exchanges, other sponsors of health benefit plans, individuals, college students, workers, labor groups, and expatriates. As of December 31, 2018, it had approximately 40 leased on-site pharmacies, 25 leased retail specialty pharmacy stores, 20 specialty mail order pharmacies, and 90 branches for infusion and enteral services; and 9,900 retail locations and 1,100 MinuteClinic locations, as well as operated an online retail pharmacy Websites, LTC pharmacies, and onsite pharmacies. The company was formerly known as CVS Caremark Corporation and changed its name to CVS Health Corporation in September 2014.

Walgreens Boots Alliance (WBA) – Walgreens Boots Alliance, Inc. operates as a pharmacy-led health and wellbeing company. It operates through three segments: Retail Pharmacy USA, Retail Pharmacy International, and Pharmaceutical Wholesale. The Retail Pharmacy USA segment sells prescription drugs and an assortment of retail products, including health, beauty, personal care, consumable, and general merchandise products through its retail drugstores and convenient care clinics. It also provides specialty pharmacy services and mail services; and manages in-store clinics. As of August 31, 2018, this segment operated 9,560 retail stores under the Walgreens and Duane Reade brands in the United States; and 7 specialty pharmacies, as well as approximately 400 in-store clinic locations. The Retail Pharmacy International segment sells prescription drugs; and health, beauty, personal care, and other consumer products through its pharmacy-led health and beauty stores and optical practices, as well as through boots.com and an integrated mobile application. This segment operated 4,767 retail stores under the Boots, Benavides, and Ahumada in the United Kingdom, Thailand, Norway, the Republic of Ireland, the Netherlands, Mexico, and Chile; and 618 optical practices, including 167 on a franchise basis. The Pharmaceutical Wholesale segment engages in the wholesale and distribution of specialty and generic pharmaceuticals, health and beauty products, and home healthcare supplies and equipment, as well as provides related services to pharmacies and other healthcare providers. This segment operates in the United Kingdom, Germany, France, Turkey, Spain, the Netherlands, Egypt, Norway, Romania, the Czech Republic, and Lithuania. The company has a strategic partnership with Microsoft Corporation.

Fundamental Overview

CVS: On November 28, 2018, CVS completed its $78 billion acquisition of Aetna, which is a healthcare insurance company. Due to this pricy acquisition, you will notice that the financials of CVS do not look good. The primary reason of this acquisition was to fend off Amazon from entering the retail pharmacy market. Although this vertical integration of CVS and Aetna looks good on paper, both companies had to agree to several conditions as part of the approval. For example, CVS and Aetna had to agree to not increase premiums as a result of acquisition costs, and keep premium rate increases to a minimum. This means that it will take CVS a long time to recover the expenses. If we compare the CVS’s 2017 and 2018 balance sheet asset line item – goodwill (goodwill is recorded after a company acquires assets and liabilities, and pays a price in excess of their identifiable value), we notice that it increased from $52 billion to $115 billion. This means that CVS overpaid by $63 billion. After nearly doubling its goodwill, CVS should expect to see losses associated with goodwill impairment. Lastly, by biting the costly bullet to integrate vertically, CVS had indirectly helped its competitors to negotiate better contracts. In other words, the other health care insurers, Pharmacy Benefit Managers (PBM), and pharmacies are going to get together in order to stay competitive after the CVS-Aetna merger. (Aside – you can think of health care insurers like your big banks, PBMs like your Visa / MasterCard / American Express, and pharmacies like the merchants whom you pay. After the CVS-Aetna merger, CVS is technically a healthcare insurer, PBM, and a retail pharmacy).

Walgreens: Last year, Walgreens bought 1,932 stores and three distribution centers from Rite Aid for nearly $4.4 billion. In contrast to CVS’s vertical integration, Walgreens-Rite Aid purchase appears to be horizontal integration. This purchase did not cause any major disturbance in Walgreens’ financials; The current ratio dropped a little since Walgreens had to use its cash (current asset) to pay for the 1,932 stores. Unlike CVS, Walgreens is sticking to its core business. On January 15, 2019 Walgreens Boots Alliance and Microsoft established a 7-year strategic partnership to transform health care delivery; The companies will combine the power of Microsoft Azure, Microsoft’s cloud and AI platform, health care investments, and new retail solutions with Walgreens’ customer reach, convenient locations, outpatient health care services and industry expertise to make health care delivery more personal, affordable and accessible for people around the world. On February 2019, Humana (medical insurer) said its joint venture with Walgreens Boots Alliance is helping boost enrollment in Medicare Advantage. On April 4, 2019, Walgreens stated that it had seen success with its Kroger partnership, and that Walgreens will move forward faster with Kroger.

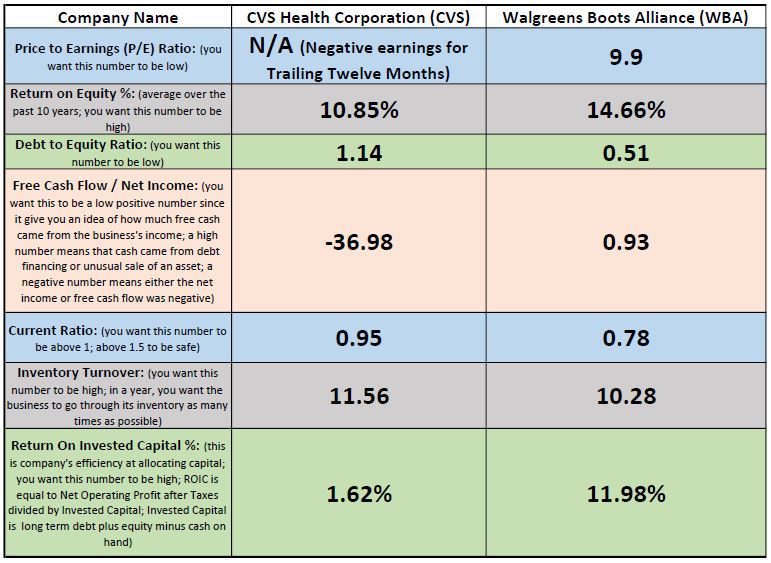

Here is the pdf version of the table above. As you can see, Walgreens surpasses CVS in every metic except the Inventory Turnover ratio. It seems that CVS is a little more efficient at going through its inventory than Walgreens is. CVS also has a better current ratio than WBA (simply because WBA had to use cash to pay for the Rite Aid stores). Walgreens has a superior P/E ratio, Return on Equity %, Debt to Equity Ratio, Free Cash Flow to Net Income, and Return on Invested Capital.

Intrinsic Value and Expected Rate of Return

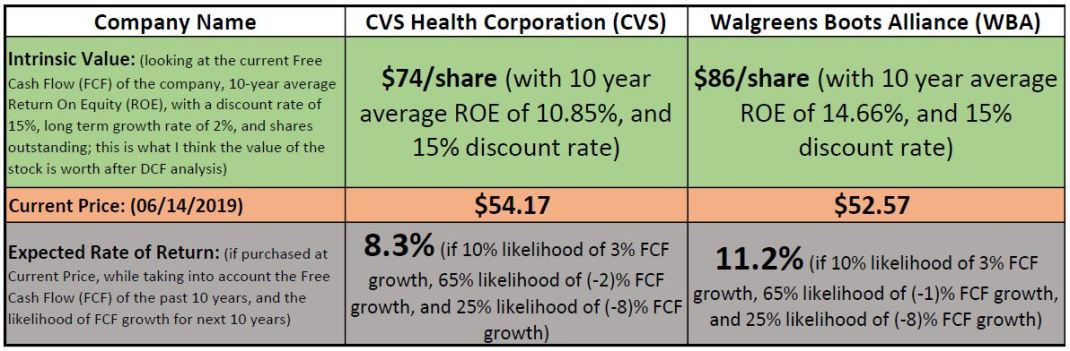

I performed a Discounted Cash Flow (DCF) analysis with a 15% discount rate. As pictured below, I found the Intrinsic Value of CVS to be $74 per share, and WBA to be $86 per share. In comparison to the intrinsic value, the current price of CVS is $54.17 per share, and WBA is $52.57 per share. So, it looks like CVS and WBA are both undervalued. However, WBA provides the highest margin of safety since the difference between its intrinsic value and current price is the greatest. Here is the PDF Version of the table below.

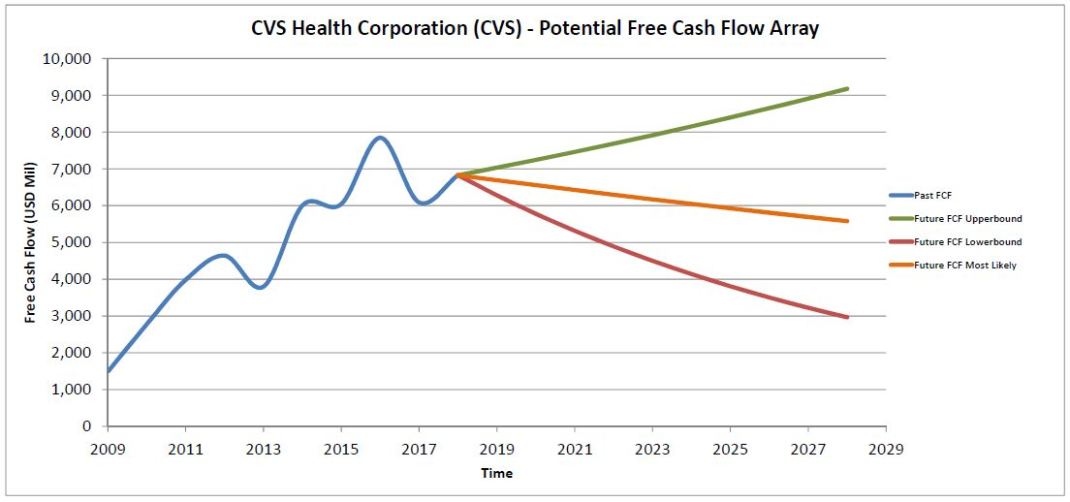

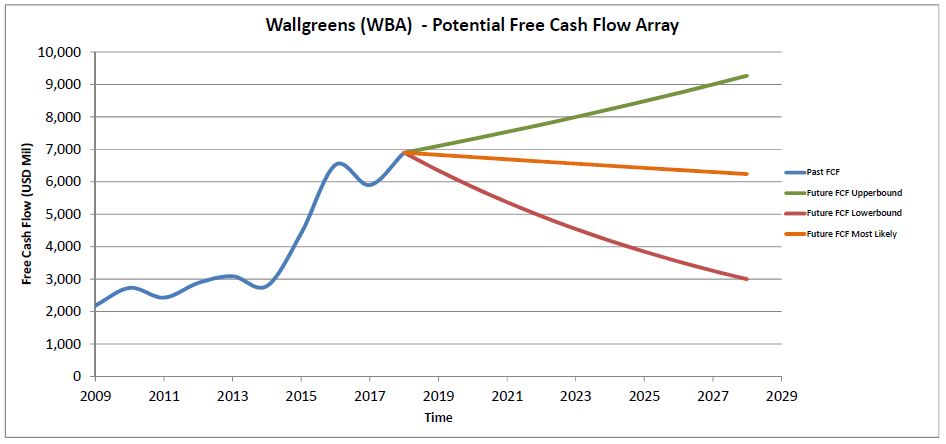

The last row in the table above is for Expected Rate of Return (RoR). If you were to invest your money at the current stock price, the expected RoR gives you an idea of what kind of annual return can you expect to get on that investment for the years to come. In other words, if you bought CVS at the current price of $54.17 per share, you could expect to see a return of 8.3%. Similarly, if you bought WBA at the current price of $52.57 per share, you could expect to see a return of 11.2%. Expected RoR takes into account the Free Cash Flow (FCF) for the past 10 years, and the likelihood of FCF growth for the next 10 years. Here are the past and projected FCF arrays along with the Upperband, Lowerband, and Most Likely assumptions for CVS and WBA:

After comparing the fundamental overview of both companies, I decided to be a little harsher on CVS while estimating its expected RoR. This is why I used a -2% FCF growth for the most likely bound for CVS. In contrast, I used -1% FCF growth for the most likely bound for Walgreens. I personally like Walgreens because it is sticking to its core business and is trying to innovate while staying within its circle of competence. Even fundamentally, Walgreens is more financially stable than CVS. As a result, if I were given a choice today to invest either in CVS or Walgreens, I would most likely pick Walgreens. Lastly, I would want to review the Annual Report (10K), especially the risks factors section, before investing in Walgreens.

Hope you learned a little and found this blog post helpful. We analyzed the two leading pharmacy chains in the United States – CVS and Walgreens. We compared various fundamental ratios, intrinsic values, and expected rate of returns. As always, you can sign up for our mailing list here. Like us on our Facebook page here. Thank you!

Email us at: superiornorthllc@gmail.com

Superior North LLC’s content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Vyom Joshi is not a professional money manager or a financial advisor. Contact a professional and certified financial advisor before making any financial decisions.