The Federal Reserve plays a key role in jump starting the economy during a downturn. As outlined on the Federal Reserve website, the Congress has directed the Fed to conduct the nation’s monetary policy to support three specific goals: maximum sustainable employment, stable prices, and moderate long-term interest rates. The Federal Reserve can achieve these goals by increasing or decreasing the money supply in the economy. In this week’s blog post, we will look at how the Fed controls the money supply, and why it is not ready for the next recession. Let’s dive in.

The Federal Reserve can increase or decrease the Federal Funds Rate, which is the interest that banks charge each other for overnight loans. By law, banks are required to have a certain percentage of their deposits in an account at the Federal Reserve, but when there is a shortfall in those accounts, banks tend to borrow from one another (Repurchase Agreement) at the interest rate set by the Federal Reserve. When Federal Funds Rate is low, it is easier for banks to borrow from one another. In contrast, when the Federal Funds rate is high, it is harder for banks to borrow because of the high interest rate associated with the principal. Even though the Federal Reserve only controls the interest rates that banks charge each other when borrowing money, those interest rate changes have ramifications that are felt by citizens and businesses all across the county. When a bank borrows money at a high interest rate from another bank, the borrowing bank has to charge a higher interest rate when it lends out the money to its customers. This means that the mortgages, auto loans, student loans, business loans, etc are all going to be at a higher interest rate. In contrast, when the Federal Funds Rate is low, the interest rates that banks charge their customers is low as well. In short, the Federal Funds Rate is directly proportional to the interest rates that banks charge their customers for various loans. Now that we understand how the Federal Reserve controls the interest rates on your mortgage/student/auto loans, let’s address the important question of why the Federal Reserve is not ready for the next recession?

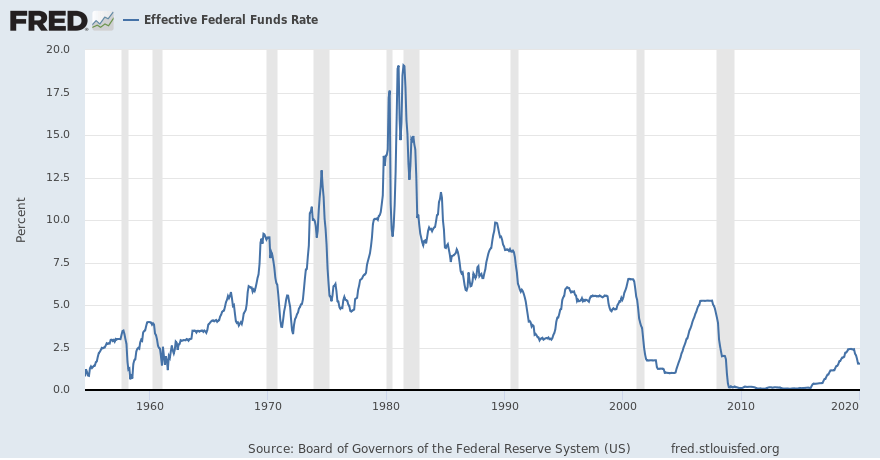

During a business cycle, every expansion is followed by a contraction (recession). For the past decade, the US economy has been expanding. This expansion has been fueled by Quantitative Easing (money printing) and near zero interest rates. When the Federal Reserve prints money, it is injecting money into the economy, which increases the money supply and simulates the economic growth. Likewise, when interest rates are near zero, it is “cheap” to borrow money, so people are more likely to borrow and spend money on that car or home, which helps jump start the economy. This is precisely what the Fed did to stimulate the economy after the Great Recession of 2007-08; The Fed cut the interest rates to near zero percent (graph below), and also injected money into the economy through Quantitative Easing.

As you can see in the graph above, the Federal Funds rate were hovering above 5% before the Great Recession. So, when the downturn rolled around, the Fed was able to bring the interest rates to near zero and make lending/borrowing very cheap and accessible. However, the Federal Funds rate in February 2020 is only 1.75%, which is really close to zero. In other words, if there was a recession around the corner, the Federal Reserve would not have the same fire power as it did back during the great recession. There was a bigger incentive to borrow and spend when interest rates were dropped from 5% to 0%, versus if the interest rates drops from 1.75% to 0%.

I do not think the Federal Reserve will ever be able to increase increase rates to those pre-crisis levels. This is simply because globally there are some central banks that offer negative interest rates – this means that the bank would pay you interest if you borrow money. With negative interest rates prevalent in some countries, it is difficult for the Federal Reserve to hike interest rates without contracting the domestic money supply and pushing the US economy into a recessionary environment. Said differently, the Federal Reserve can not prepare itself for the next recession by increasing interest rates without actually contracting the economy and pushing the United States into a recession. The access to “cheap” low interest money has been around for more than a decade, so borrowers have become so used to it that even a slight increase in the interest rates pushes the Repo rates through the roof, which is what happened in September 2019.

After the great recession, to further increase the money supply in the economy and stimulate growth, the Federal Reserve printed money out of thin air. Contrary to popular belief, this money creation did not really cause a lot of inflation. However, I believe all the money that was injected likely ended up creating a stock market bubble or a student loan/debt bubble. Similar to the post crisis quantitative easing, the Federal Reserve might have to resort to quantitative easing during the next recession. This isn’t ideal because it does erode the value of dollar. In other words, you are penalized to save money in your bank account.

I do not know precisely when the next recession will be, but I know for a fact that there will be a recession in the near future, and the Federal Reserve is not ready for it. Due to globalization, there are many international events which could affect the US economy, and push the United States into a recession. Dropping the interest rates from 1.75% to 0% will not be enough to bring the world’s largest economy out of a recession.

Hope you learned a little and found this blog post helpful. We talked about the role the Federal Reserve plays during a recession, and why the Federal Reserve is not ready for the next recession. As always, you can sign up for our free mailing list here. You can sign up for our paid subscription services here. Like us on our Facebook page here. Thank you!

Superior North LLC’s content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Vyom Joshi is not a professional money manager or a financial advisor. Contact a professional and certified financial advisor before making any financial decisions. Please review the Disclaimer and Terms and Conditions.