Wells Fargo is an American financial company, which has had some backlash due to its account fraud scandal. Is this a big enough hole for you to abandon the WFC ship and hop over to another ship? Or are you the person you believes in second chances?

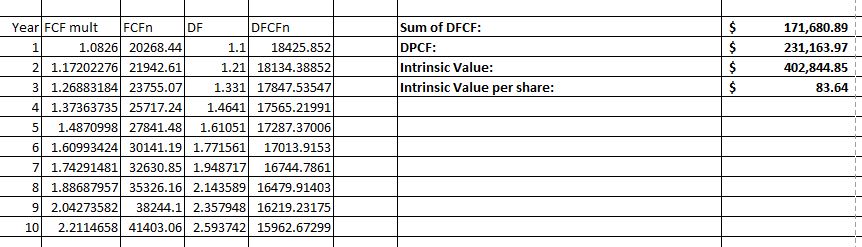

When a perform a DCF calculation with the below assumptions, I find that the intrinsic value of WFC is $83.64/share. The current price of WFC is hovering around $59/share.

So, according to my 10% discount rate, it looks like WFC is undervalued. WFC’s Debt to Equity ratio is 1.22, which is a little bit higher than JPM’s Debt to Equity ratio of 1.16. Even though WFC’s P/E ratio is 15, which is lower than the industry average and the S&P 500 average, you still need to look at other figures before you consider it a buy. Wells Fargo’s Price to Cash Flow ratio is 12.0, compared to the industry average Price to Cash Flow ratio of 8.7.

Looking at the past 10 years of Earnings Per Share (EPS), we can see that there has been a steady growth from an EPS of 0.7 is 2008 to 4.10 in 2017. I think that WFC is strong and has good potential. It is definitely a good investment. Furthermore, given the fact that WFC recently got some bad publicity, they are more likely to correct their actions and not do it again. What do you think about investing in Wells Fargo? Worth it or not?

Check out our Facebook page here.

Sign-up on our Mailing List here.

Email us at: superiornorthllc@gmail.com