I was recently reading about the Micra pacemaker, which is one of the many medical devices manufactured by Medtronic. Micra is one-tenth the size of its competing models, and attached directly to the heart. This means there are no wire leads that can cause an infection, and there is no need to create room in the chest for this device. Even though Micra costs 3 times as much as competing pacemakers, Micra takes up 60% of the market. With such cutting edge technology, Medtronic became my research topic. In this week’s blog post, I will talk about the world’s largest medical devices company – Medtornic.

Company Overview

Medtronic plc develops, manufactures, distributes, and sells device-based medical therapies to hospitals, physicians, clinicians, and patients worldwide. It operates in four segments: Cardiac and Vascular Group, Minimally Invasive Therapies Group, Restorative Therapies Group, and Diabetes Group.

The Cardiac and Vascular Group segment offers implantable cardiac pacemakers, cardioverter defibrillators, and cardiac resynchronization therapy devices; AF ablation products; insertable cardiac monitor systems; mechanical circulatory support; TYRX products; and remote monitoring and patient-centered software. It also provides aortic valves; percutaneous coronary intervention stents, surgical valve replacement and repair products, endovascular stent grafts, percutaneous angioplasty balloons, and products to treat superficial venous diseases in the lower extremities.

The Minimally Invasive Therapies Group segment offers surgical products, including surgical stapling devices, vessel sealing instruments, wound closure, electrosurgery products, hernia mechanical devices, mesh implants, and gynecology products; hardware instruments and mesh fixation device; and gastrointestinal, inhalation therapy, and renal care solutions.

The Restorative Therapies Group segment offers products for spinal surgeons, neurosurgeons, neurologists, pain management specialists, anesthesiologists, orthopedic surgeons, urologists, colorectal surgeons, urogynecologists, interventional radiologists, and ear, nose, and throat specialists; and systems that incorporate energy surgical instruments. It also provides image-guided surgery and intra-operative imaging systems and robotic guidance systems used in robot assisted spine procedures; and therapies for vasculature in and around the brain.

The Diabetes Group segment offers insulin pumps and consumables, continuous glucose monitoring systems, and therapy management software.

Fundamental Overview

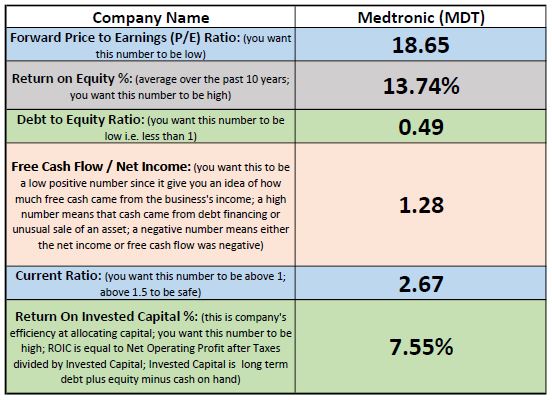

At the current price of $112.06/share, Medtronic has a forward P/E ratio of 19, and a forward dividend yield of about 2%. MDT has 10-year average Return On Equity (ROE) of 13.74%, which shows that management is efficiently using company’s assets to create profit. The debt to equity ratio is 0.49, which shows that Medtronic’s debt is under control. The free cash flow to net income is 1.28, which has remained fairly consistent over the past 10 years. MDT’s current ratio is 2.67, which indicates that Medtronic has 2.67 times more current assets than its current liabilities. The Return On Invested Capital (ROIC) is 7.55%, which is expected to be less than ROE (13.78%) because ROIC takes into account the company’s debt along with its equity (i.e. ROIC has a larger denominator than ROE). Here is the pdf version of these 6 ratios below.

Warren Buffett prefers Debt to Equity ratio of 0.5 or lower, current ratio above 1.5, and ROE consistently above 8% over a 10 year period. MDT passes these 3 requirements with flying colors. Although a forward P/E of 19 is a bit high for a value investor, P/E of 19 is considered fairly low given the large moat Medtronic has in the medical devices industry. Medtronics has consistently paid dividends, and has had steady EPS numbers over the past 10 years. In today’s market, when the stock market is at an all time high, I believe that a forward P/E of 19 for Medtronic is a bargain.

Intrinsic Value and Expected Rate of Return

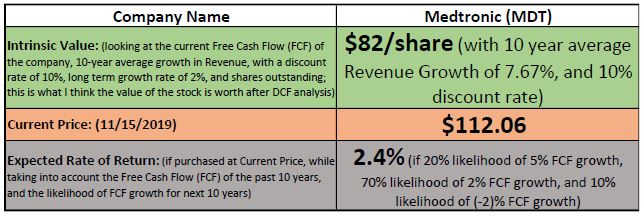

I performed a Discounted Cash Flow (DCF) analysis with a 10% discount rate. As pictured below, I found the Intrinsic Value of MDT to be $82 per share. In comparison to the intrinsic value, the current price of Medtronic is $112.06 per share. So, it looks like MDT is trading at a premium of 36% above its intrinsic value. Here is the pdf version of the table below.

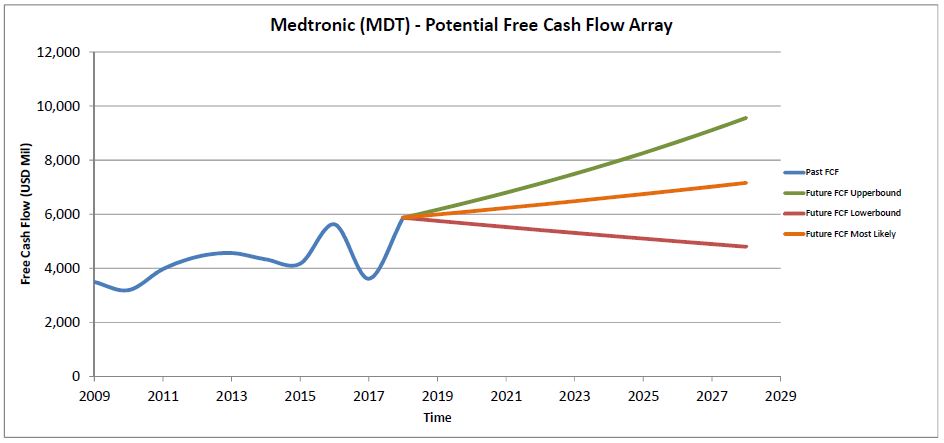

The last row in the table above is for Expected Rate of Return (RoR). If you were to invest your money at the current stock price, the expected RoR gives you an idea of what kind of annual return can you expect to get on that investment for the years to come. Expected RoR takes into account the Free Cash Flow (FCF) for the past 10 years, and the likelihood of FCF growth for the next 10 years. Here are the past and projected FCF arrays along with the Upperband, Lowerband, and Most Likely assumptions for Medtronic:

When we compare the intrinsic value and the current stock price, we notice that there is no margin of safety. Ben Graham would probably shy away from this investment, but given the fundamentals and the growth prospect of Medtronic, I am reminded of Charlie Munger’s quote: “Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return—even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with a fine result.” In other words, it is fine to pay a premium if the stock has great potential for growth. Furthermore, with its low volatility in stock price and steady earnings, MDT is also a good pick for defensive investment. Moreover, Medtronic is expected to grow at a faster rate than the other defensive investments such as utilities and consumer staples. In conclusion, Medtronic is a stock worth having in your portfolio. ![]() Hope you learned a little and found this blog post helpful. We analyzed the world’s largest medical device company: Medtronic (MDT). We looked at various fundamental ratios, intrinsic values, and expected rate of returns. As always, you can sign up for our free mailing list here. You can sign up for our paid subscription services here. Like us on our Facebook page here. Thank you!

Hope you learned a little and found this blog post helpful. We analyzed the world’s largest medical device company: Medtronic (MDT). We looked at various fundamental ratios, intrinsic values, and expected rate of returns. As always, you can sign up for our free mailing list here. You can sign up for our paid subscription services here. Like us on our Facebook page here. Thank you!

Superior North LLC’s content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Vyom Joshi is not a professional money manager or a financial advisor. Contact a professional and certified financial advisor before making any financial decisions. Please review the Disclaimer and Terms and Conditions.